Oklahoma State Treasurer Todd Russ

By Todd Russ, Oklahoma Treasurer

PORTFOLIO PERFORMANCE, DIVERSIFICATION, AND STRATEGY

November portfolio yielded 3.71%, up from 3.43% last year, with a weighted average maturity of 758 days.

Total assets under management of $17.2 billion, up $1.5 billion in comparison to November 2024.

Total portfolio contained 66.9% in U.S. Treasurys, 0.4% in U.S. government agencies,

19.2% in money market mutual funds, 12.2% in mortgage-backed securities, 0.4% in certificates of deposit,

and 0.7% in state and foreign bonds, comprising the balance of funds invested.

TOTAL FUNDS INVESTED

Funds available for investment at market value include the State Treasurer’s investments at $11,631,306,537 and State Agency balances in OK Invest at $3,707,993,474, American Rescue Plan investments at $828,490,234, and the Oklahoma Capitol Improvement Authority Legacy Fund at $974,950,635, Oklahoma Capital Assets Maintenance and Protection Fund at $124,215,195 for a total of $17,539,768,852.

MARKET CONDITIONS

Treasury yields continued to trend lower through November as investors reinforced expectations for Federal Reserve rate cuts amid signs of moderating growth and cooling inflation pressures. The 2-year Treasury closed the month at approximately 3.49%, down from 3.58% at the end of October, while the 10-year benchmark finished near 4.02%, down from 4.07%. Declines were most pronounced at the front end of the curve, resulting in a modest steepening as longer-dated yields remained comparatively stable.

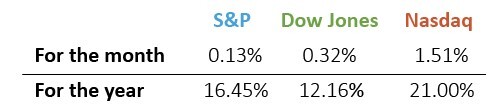

Equity markets delivered mixed performance in November as leadership rotated away from growth-oriented sectors. Despite the softer monthly tone, year-to-date equity performance remained firmly positive. The Nasdaq Composite continued to lead, reflecting resilient equity markets despite near-term volatility and shifting policy expectations.

The October 28–29 FOMC minutes, released November 19, showed rising disagreement over further easing after the Fed cut rates 25 basis points to 3.75%–4.00%, citing slowing job growth but lingering inflation above the 2% target.

On December 10, 2025, the Federal Reserve implemented another 25-basis point cut, lowering the federal funds target range to 3.50%–3.75%. According to the Federal Reserve’s December policy statement, the decision reflected moderating economic activity, slowing job gains, and a rise in downside risks to employment, while maintaining a data-dependent approach to future policy adjustments.

ECONOMIC DEVELOPMENTS

The unemployment rate rose to 4.6% in November from 4.4% in September, the highest level in more than four years, as the labor market continued to cool following a weak October that was not separately reported due to the federal government shutdown. According to the Bureau of Labor Statistics (BLS), nonfarm payrolls increased by 64,000 in November, following a 105,000 job decline in October, with job gains led by health care and social assistance and losses concentrated in transportation and warehousing, leisure and hospitality, and federal government employment. Labor market slack increased further, with rises in long-term unemployment and workers employed part time for economic reasons, while higher labor force participation contributed to the uptick in the unemployment rate, reinforcing evidence of a gradually cooling labor market.

The Consumer Price Index (CPI) eased further in November, with headline inflation rising 2.7% year over year, down from 3.0% in September and below economists’ expectations of 3.1%. According to the Bureau of Labor Statistics, core CPI increased 2.6% annually, slowing from 3.0% previously and marking the slowest pace since early November 2021. Energy prices rose 4.2% year over year, driven by an 11% increase in gasoline prices and a 7% rise in electricity, while food prices advanced 2.6%. Inflation in services moderated, with shelter costs up 3.0% year over year, the smallest increase in more than four years, while declines in airfares, hotel stays, recreation, and apparel prices helped restrain underlying price pressures.

The Bureau of Labor Statistics did not release Producer Price Index (PPI) data for October, and no updated figures were published in November due to disruptions from the federal government shutdown. The most recent data show PPI rose 0.3% month over month in September, matching expectations and rebounding from a 0.1% decline in August, according to the BLS release issued on November 25.

Retail sales were unchanged in October (0.0%), following a 0.1% increase in September, falling short of economists’ expectations for a 0.1% gain. According to the U.S. Department of Commerce, sales excluding autos and gasoline rose 0.5%, while control-group sales, which feed directly into GDP calculations, increased 0.8%, the strongest monthly gain in four months. Motor vehicle sales declined 1.6%, weighing on the headline figure, while spending strengthened at online retailers, department stores, and electronics and appliance stores, indicating underlying consumer demand remained resilient despite slowing overall momentum.

Existing-home sales rose 0.5% month over month in November to a seasonally adjusted annual rate of 4.13 million units from 4.10 million units, marking a third consecutive monthly increase, according to the National Association of Realtors (NAR). Sales declined 1.0% year over year, while the median existing-home price increased by 1.2% to $409,200, extending annual price gains to 29 straight months. Housing inventory fell 5.9% from October’s 1.52 million units to 1.43 million units, representing a 4.2-month supply. NAR Chief Economist Lawrence Yun noted that lower mortgage rates supported sales activity, though inventory growth has begun to stall, limiting affordability improvements.

The full third-quarter 2025 estimate for real gross domestic product (GDP) from the Bureau of Economic Analysis (BEA) has not been released yet, due to the government shutdown. The second quarter remains the most recent official data, showing real GDP growth of 3.8% annualized, driven by lower imports and stronger consumer spending, while investment and exports declined.

COLLATERALIZATION

All funds under the control of this office requiring collateralization were secured at rates ranging from 100% to 110%, depending on the type of investment.

Get Local News!